As I travel around and visit many different places, the disparity in the speed at which the credit crunch is unfolding in different places is readily apparent, and with it the attitudes of local people to warnings of hard times to come. In places where the bursting of the credit bubble is more advanced, such as Ireland, people are generally more interested in understanding what went wrong and what they can do for themselves and their communities. In such places, where homes may already only be worth 40% of the mortgage on them, there is more public recognition and discussion of the issues, even if there is still a great deal of collective denial.

In other places where the impact of the bubble has yet to be felt, for instance Canada, where I am currently, there is still a sense of invulnerability. We haven’t got as far as denial yet. That’s hardly surprising when you can’t tell a crack-shack from a mansion in places like Vancouver. This is bubble psychology at its most extreme, where no one cares what they pay for something, because they think someone else will always pay more, and no one cares what they owe, so long as the monthly payment is manageable in the short-term. Most other Canadian cities are still in the grip of bubble psychology as well, although not to the same extent. Needless to say, the level of public discussion in Canada is abysmally low.

The psychological contrast between Ireland and Canada is stark indeed. Ireland had one of the worst housing bubbles in the whole world. When I used to spend a lot of time there in the early 1990s, it was a sleepy agricultural place where no one seemed to have two cents to rub together, but they were the happiest people I knew. Interest rates had always been relatively high, so borrowing large amounts of money was not affordable. People had no access to the cheap credit that allows purchasers to bid up property prices with gay abandon. Access to land ownership had always been quite limited, with ownership concentrated in relatively few hands. Divorce was not only illegal, but unconstitutional, partly to avoid the break up of land parcels.

Irish property prices were a fraction of what they were in most parts of England at the time. In fact, local authorities in England were trying to escape their duty to house their own populations in council properties by buying them a cheap house in Ireland, instead of continuing to rent them one in England. The maintenance bill for decrepit council housing was so large that buying council tenants off with an Irish house made financial sense.

When Ireland joined the eurozone, interest rates plummeted to levels the Irish hadn’t seen before. All of a sudden, people had access to cheap credit, and the EU pumped in enormous amounts of money (some 17 billion euros since the advent of the euro) for upgrading infrastructure. The Celtic Tiger was born, and the long-standing Irish diaspora went into reverse, with the addition of a wave of new immigration from Eastern Europe.

What followed was a staggeringly large property bubble, fuelled by extremely cheap credit that gave rise to almost insatiable demand. Property prices rose by a factor of 15 in 15 years. For a few years, the Irish were called the second richest people in the world (after Icelanders, who had managed to turn their entire country into a hedge fund in an even bigger credit boom). This is not riches, however. This is simply accumulating a veneer of material prosperity at the cost of digging oneself into an inescapable debt trap.

Since the Irish real estate bubble peaked and burst in 2007/2008, prices have plummeted and the Irish banking system has been plunged into crisis. The state guaranteed all deposits – a promise which it could not possibly afford to keep in reality. It pumped some 22 billion euros into a bank bailout (far more in one fell swoop than all the funds pumped in by the EU since Ireland joined, making EU membership a net negative for Ireland). With the scale of the banking woes becoming increasingly obvious, the government set up NAMA (the National Asset Management Agency) in 2009, with a view to using taxpayers’ money to assume ownership of troubled property assets:

The idea is that the NAMA “will buy all of the land and property development loans of the six Irish banks of covered by the State guarantee. This means the total potential value of the loans which will be taken on by NAMA will be between €80 billion and €90 billion. By taking problem property loans off the hands of the banks, the Government hopes to put those institutions in a position where they can resume lending.

NAMA will probably become the biggest landowner in Ireland. Developers might not yet realise it – but every single land and investment property they own which has outstanding debt could end up in the new National Asset Management Agency. Even if these debts are bought by Nama at two-thirds of their face value – the bill could be in the region of €60 billion. (Ireland’s national debt is currently €54 billion.)”

This is a monumental transfer of public assets into private hands through a privatized-profits-but-socialized-losses model. The concentration of property ownership in Ireland is returning with a vengeance. With ordinary people having spent unpayable amounts to buy real estate, they are now likely to forfeit their property to the wealthy, who will buy it up from NAMA at a few eurocents on the euro.

This is the property ownership model that gave Ireland the great famine (an Gorta Mór – the Great Hunger of 1845-1852), when wealthy landowners continued to export food while half the tenant population either starved or emigrated. The population is still nowhere near what it was in 1850 as a result. Highly concentrated property ownership, with its concurrent gridlock on political power, risks an isolated elite acting purely in its own short-term interests, no matter what the consequences to the rest of the population.

It is quite possible, indeed likely, that Ireland (and other highly indebted states of the European periphery) may leave the eurozone, causing an enormous wave of economic dislocation, which would compound the impact of on-going credit crunch. While I don’t see the periphery being forced to leave by other member states, I do see the austerity measures required to remain part of the club becoming so onerous that implementing them domestically would become a recipe for political suicide. Leaving the eurozone is no panacea though. Ireland is inevitably looking at a long period of extreme socioeconomic and political upheaval no matter what decisions its politicians make now.

Canada should be looking at Ireland for lessons on what the bursting of a major real estate bubble looks like, and the consequences of personal indebtedness. We too, over many years, have thrown caution to the wind when it comes to being offered the ‘opportunity’ to dig ourselves in over our heads:

Canadians’ Personal Debt at Historic Level

As interest rates drifted to the lowest levels in decades, consumers responded by buying everything from homes and cottages to cars and appliances. The shopping spree has fed a healthy cycle of economic growth and a robust job market – but we’ve gone deep into hock to pay for the good times. With every drop in interest rates, the definition of living within one’s means changed – with financing like this, you too can afford a luxury condo! The notion of buying only what you could easily pay for became a meaningless principle.

Personal debt in Canada has been described as a Ticking Time-Bomb:

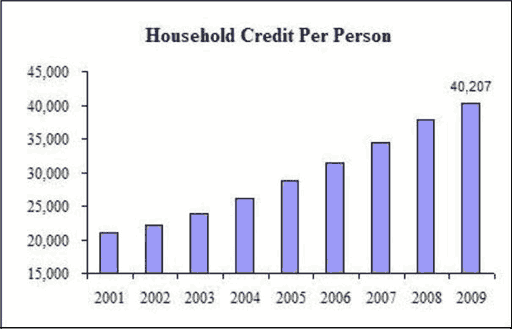

As the chart shows, back in the year 2000 we each had approximately $20,000 in debt, so in less than a decade the debt we are carrying has doubled. That’s a staggering statistic. If you are the average Canadian, your debt has doubled. Has your income doubled? Are you making twice as much today as you were earning in the year 2000? Probably not. If you still have a job you may have received “cost of living” increases of 2% per year for the last decade, but that obviously does not add up to a doubling of your income.

Canadians are extremely vulnerable, but do not seem to realize it:

Average Canadian household debt reaches $96,000

The average Canadian family’s household debt rose to $96,000 last year, a new study says. Debt-to-income levels rose to 145 per cent – the highest level ever recorded in the study, which has run annually for 11 years. The Vanier Institute of the Family study found a dramatic rise in late debt payments. Mortgage payments that were at least 90 days late were up 50 per cent over 2008.Additionally, there was a rise of 40 per cent in credit card payments that were three months behind. The study said first-time mortgage buyers were taking on the most debt, unsurprisingly. However, the study says that many have taken advantage of record low interest rates and may have problems making payments if interest rates rise. Two-thirds of Canadians 18-34 would find themselves in trouble if their paycheque was delayed by only one week, a September 2009 survey by the Canadian Payroll Association found.

Canadians should also be looking south of the border, at the skyrocketing foreclosures in former bubble areas, despite a year-long rally in the credit markets. They should be looking at the inventory build-up that has already exceeded the crisis period of 2008, and continues to reach for the sky now that the credit markets have turned down again. Where the credit markets lead, the real economy will follow. If people cannot get financing, there will be no price support for real estate at anything like current housing prices.

Canadians should not be listening to MSM coverage of ‘green shoots of recovery’. Those ‘green shoots’ are gangrene. The MSM, along with governments and central bankers, have been playing confidence tricks on the public for a long time. They are trying to convince people that there is nothing to worry about, that they should just go back to spending-in-their-sleep, as has become a well-entrenched habit.

Canadians need to wake up and look at the world around them – at where Ireland already is, and where much of the rest of Europe and the US are heading very quickly. To imagine that Canada can remain immune from tectonic shifts in the global economy is the height of folly. We are beginning to see some mention of Canadian housing bubbles, but the message is heavily downplayed by those who are prepared to mention it, and has not yet begun to sink in among the general population at all.

Housing prices due to fall, says think-tank

Canada’s major metropolitan housing markets are looking awfully bubbly and are due to burst, says a report released Tuesday. The report, entitled Canada’s Housing Bubble: An Accident Waiting to Happen, by the Canadian Centre for Policy Alternatives, looks at prices in Toronto, Vancouver, Calgary, Edmonton, Montreal and Ottawa. It concludes that housing price appreciation is frothy in comparison to historic values.“I think at best you will see stagnation in housing prices or some kind of correction, and at worst you will see the bubble bursting,” said David Macdonald, an economist and research associate at the centre.

Housing bubbles emerge when prices increase more rapidly than inflation, household incomes and economic growth. That has been the case for Canada over the last run-up in prices, according to the report.

Macdonald said this bubble is different than others, because for the first time it is spreading beyond Toronto and Vancouver.

“Canada is experiencing for the first time in 30 years a synchronized housing bubble across the six largest residential markets,” he said. [..] Macdonald gives three scenarios in which prices might drop.

- The first is similar to what happened in Vancouver in 1994, a market correction through price deflation. In that scenario, Toronto prices would decline by 9 per cent from an average of $420,000 to $382,000.

- In the second scenario, the bubble would burst more slowly, similar to the 1989 Toronto bubble. In that case, prices would decline by 21 per cent from $420,000 to $330,000 over a five-year period.

- In the worst scenario, a bubble would form similar to the United States and prices would fall rapidly. In that case Toronto prices would drop 20 per cent over three years to $335,000. The price drop would be slightly less than in scenario two, but happen more rapidly.

“Bringing house prices down just enough to moderate expectations but not so much as to cause a panic is a delicate balance,” says the report. “Government policy makers, the Bank of Canada, as well as rate setters at the big banks need to work together to steer the Canadian market to a soft landing. The alternative is not acceptable.”

Reality does not care what people find acceptable. Reality does not negotiate, it dictates. Real estate has further to fall here than almost anyone can image, as every bubble is followed by a substantial undershoot. Even as far as Ireland has fallen, or bubbly parts of the US, there is much further to go to approach pre-bubble prices, and the property crunch will take them much further than that. Canada has not even begun the extremely painful real estate deleveraging process. We have a very long way to fall indeed.